Call Today!

(239) 234-9717

Life Insurance

Life Insurance is Like a Security Blanket for Your Loved Ones. Provides ready money to the people who depend on your paycheck, should you pass away.

Think of life insurance like a security blanket that can help financially protect the people you love most.

Do I Need Life Insurance?

Some people wait for a major life event to buy life insurance — a wedding, a new home, or a newborn. But the most important thing about life insurance is buying it before you need it.

It’s not exclusively for those who are married or have children either. If anyone is dependent on you financially, such as an aging parent, life insurance is a must. Not sure if you need it? See if you fit into any of the following categories:

You’re married

You have a domestic partner

You have a spouse and kids

You’re the primary breadwinner

You’re single with kids

You have a home

You own your business

You have student loan debt

You’re retired

If this sounds like you, it may be time to buy life insurance.

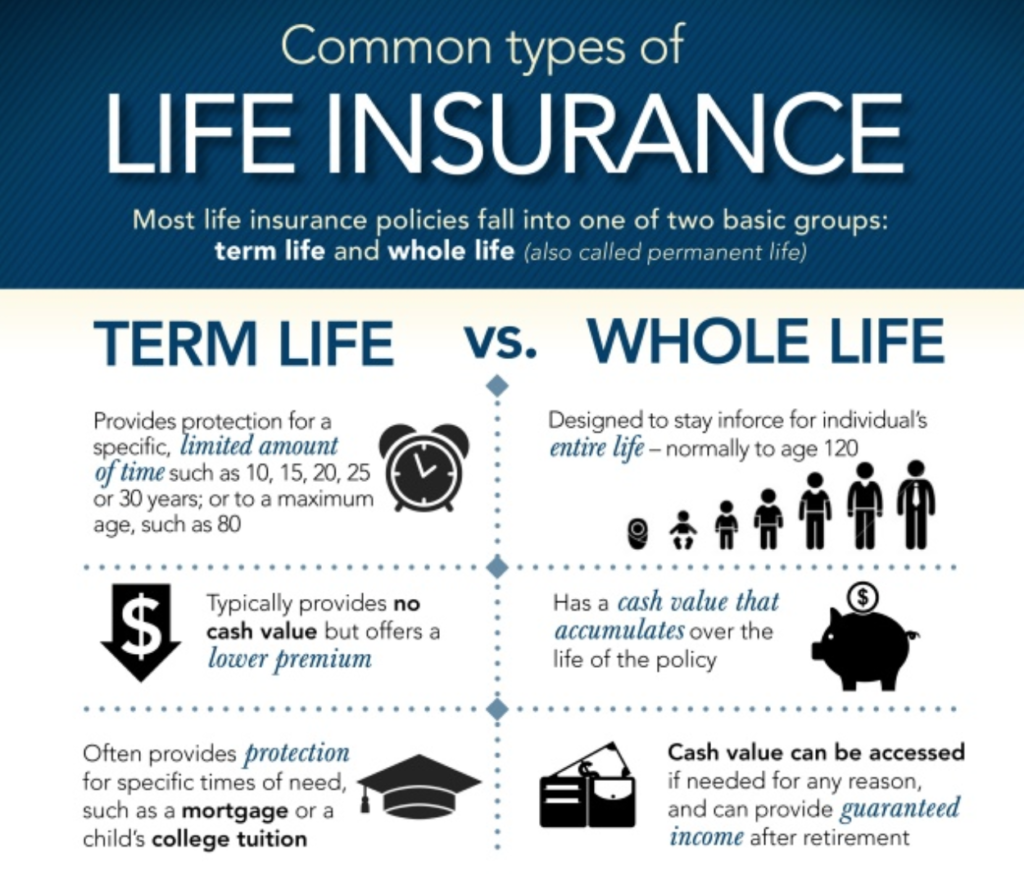

What Type of Life Insurance Do I Need?

There are two main types of life insurance policies to consider: term and whole life insurance.

Term life insurance offers protection for a set period of time, or a “term.” As the policyholder, you can choose your term, typically between 10 to 30 years. It’s often the less expensive of the two options, as term life insurance policies come with an expiration date. Once that term ends, so does your coverage. It’s best for those who have greater coverage needs for a certain period of time, such as while your family is still growing.

Whole life insurance, on the other hand, lasts for a lifetime (subject to payment of premiums, and terms of conditions of policy). With each payment you make, a portion of it is set aside for a rainy day, which becomes your policy’s “cash value.” If your car breaks down or you have an unforeseen medical expense, you can borrow against your policy’s cash value, often at a favorable rate.

Benefits of term life insurance

There are several types of life insurance, but the most popular type, and the one that makes sense for most people, is term life insurance, which you buy to last until your debts are paid off (generally a 20- to 30-year term).

The benefits of a term life plan include:

Benefits of Whole Life Insurance

Alternatively, whole life insurance is a permanent insurance product that combines investing and life insurance. Once you buy a policy, as long as you continue to pay premiums (or build up enough cash value to cover the premiums), you are covered until you die. Whole life insurance can cost four times the amount of term life insurance, but it also has its own benefits:

- Term insurance is easy to understand.

- Term life insurance is the cheapest life insurance you can buy.

- If you buy term life insurance when you’re young, you can lock in low rates.

- Term life insurance is purely an insurance product and doesn’t have a savings or investment component. This is a good thing — you can increase your returns by investing and saving on your own.

- If you have a term life policy and can no longer afford it, you won’t lose anything more than the premiums you’ve paid if you decide to abandon the policy.

- Combines life insurance with an investing component.

- The cash-value component can be used as part of a complex estate-planning strategy.

- Works as a forced savings vehicle.

- You can often take out loans against the cash-value portion, although this could decrease your death benefit.

Frequently Asked Questions

Do I need life insurance?

As a general rule, if you’re the primary breadwinner of the house and there are people who depend on you for financial support, like a spouse, children, or aging parents, then you’re a good candidate for life insurance. Additionally, if you have debt that another person will have to assume, like a mortgage or student loan debts, it’s a good opportunity to look into life insurance.

What is a beneficiary?

The beneficiary is the person or entity named as the recipient of your policy’s death benefit. It can be a family member, a person unrelated to you, or even a business or other organization. You choose the beneficiary on your own—you don’t need permission from the insurer or the beneficiary. You can also choose more than one beneficiary, and designate how you want the death benefit to be split among them.

Your insurer will automatically disburse the death benefit if you die, but it’s still a good idea to tell any beneficiary about the policy so he or she will be prepared to take action should a problem arise. For this same reason it’s also a good idea to provide the beneficiary with access to the contract.

Does a beneficiary need to do anything to receive the death benefit?

Technically a beneficiary does not have to do anything to receive your policy’s death benefit, but it’s a good idea to make sure he or she is aware that the policy exists in case there are any delays or complications on the insurer’s side.

The insurer will require proof of death and a copy of the contract in order to disburse the benefit.

Are my life insurance premiums tax deductible?

The premiums you pay for your life insurance policy are not tax deductible.